In the ever-evolving landscape of personal finance and housing, the age-old debate of buying versus renting a home remains as relevant as ever, especially in 2025 amid fluctuating mortgage rates, rising rents, and shifting economic priorities.

As of July 2025, with average 30-year fixed mortgage rates hovering around 6.74%, and national rent increases projected at 0.8% to 6% year-over-year depending on unit type and location, the decision hinges not just on raw numbers but on your financial profile, lifestyle aspirations, and long-term vision.

This comprehensive guide explores the nuances of buying versus renting, starting with high spending power individuals or couples—who often leverage homeownership for wealth amplification—and progressing to middle- and lower-income scenarios, where flexibility and affordability take precedence.

We’ll examine key factors like equity building, tax incentives, maintenance burdens, market dynamics, and lifestyle implications, drawing on current 2025 data to provide a balanced, high-level perspective. Whether you’re a high-net-worth executive eyeing a luxury estate or a budget-conscious family navigating urban rentals, this analysis aims to empower you with insights tailored to your circumstances.

Remember, while buying often emerges as a path to long-term stability and wealth in many markets, renting frequently offers immediate cost savings and mobility—saving an average of $908 per month on starter homes in top metros. Ultimately, the “better” choice is deeply personal, influenced by your horizon: short-term flexibility or enduring investment?

For High Spending Power Individuals or Couples: Leveraging Ownership for Wealth and Legacy

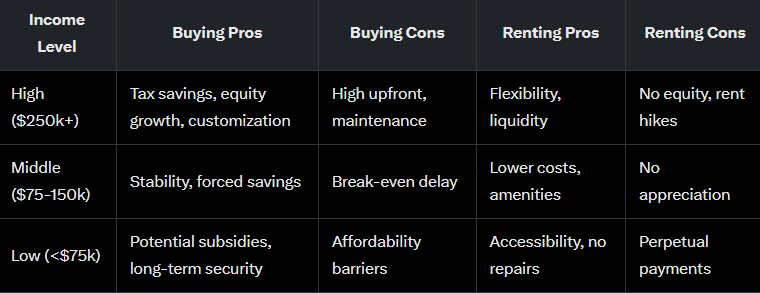

For affluent individuals or couples—those with annual incomes exceeding $250,000, substantial savings, and access to premium financing—buying a home in 2025 often aligns seamlessly with strategies for wealth preservation and growth. High earners, such as tech executives in Silicon Valley or finance professionals in New York, benefit disproportionately from homeownership’s financial levers, particularly in a market where property appreciation in desirable areas outpaces inflation.

Let’s break this down at a high level.The Equity and Investment Edge: Purchasing a high-end property allows you to build significant equity over time. For instance, a $2 million home with a 20% down payment ($400,000) and a 6.74% mortgage rate results in monthly payments around $10,300 (principal and interest), but as you pay down the loan, your ownership stake grows. In appreciating markets like coastal California, where home values have risen 4-6% annually despite broader slowdowns, this equity can compound into millions, serving as collateral for lines of credit, investment loans, or even funding ventures.

Renting a comparable luxury apartment or estate might cost $15,000+ monthly in elite neighborhoods, but that money vanishes into a landlord’s pocket, offering no return beyond immediate use. For high spenders, buying transforms housing from an expense into an asset class, potentially yielding capital gains upon sale—tax-free up to $500,000 for couples under current rules.Tax Advantages Amplified:

Homeownership’s tax benefits shine brightest for the wealthy. In 2025, you can deduct mortgage interest on up to $750,000 of debt for primary or secondary homes, potentially saving tens of thousands annually in high-tax brackets (e.g., 37% federal rate). Property taxes are deductible up to $10,000 under the SALT cap, and energy-efficient upgrades qualify for credits via the Inflation Reduction Act extensions.

For a couple in a $3 million home, these deductions could offset $50,000+ in taxable income, far outweighing rental perks. Renting offers no such offsets; instead, high-end rentals in 2025 face upward pressure from 5-6% increases in premium markets, eroding disposable income without building net worth.

Lifestyle and Stability Perks:

Affluent buyers often prioritize customization and privacy—renovating a purchased property to include home theaters, smart systems, or eco-features without landlord approval. In a stable 2025 market with low sales volume (hitting 30-year lows), buying locks in fixed mortgage payments, shielding against rent hikes that could add $10,000+ yearly to luxury leases. However, cons include hefty upfront costs (closing fees, inspections) and maintenance—though high earners can outsource this via property managers.

Renting appeals for globe-trotting executives, offering turnkey luxury with amenities like concierge services in high-rises, but it lacks the legacy of passing down a family estate.In summary, for high spending power profiles, buying in 2025 often “wins” for wealth amplification, with studies showing homeownership still more affordable long-term in 70% of U.S. markets despite high rates. Yet, if your lifestyle demands frequent relocations or you prefer investing capital elsewhere (e.g., stocks yielding 8-10% returns), renting preserves liquidity.

For Middle-Income Families: Balancing Affordability and Aspirations

Transitioning to middle-income earners—households with $75,000-$150,000 annual income, such as teachers, mid-level managers, or dual-earner families—the calculus shifts toward practicality in 2025’s challenging market. Here, renting frequently edges out as the short-term winner due to elevated borrowing costs, but buying retains appeal for those planning 5+ years in one place.

Cost Dynamics and Break-Even Points: A typical $400,000 home requires a $80,000 down payment and monthly payments of about $2,600 at current rates, plus $500-800 in taxes/insurance—totaling $3,200. Comparable rentals average $2,296 nationally, saving $900+ monthly initially. Over three years, renting could save $27,648, but buying breaks even after 5-7 years via equity and fixed payments amid 4-5% rent hikes. In buyer-friendly cities like Detroit or Cleveland, buying is cheaper upfront, while in pricey metros like San Francisco, renting dominates.

Pros of Buying:

Stability and Growth: Middle earners value the forced savings of mortgage payments, building equity that cushions against inflation. Tax deductions on interest (up to $750k debt) and property taxes ($10k cap) provide $5,000-10,000 annual relief, and programs like FHA loans reduce down payments to 3.5%. Ownership fosters community roots, ideal for families with school-aged children.Renting’s

Flexibility Appeal: No down payment burden means more savings for emergencies or investments. Landlords handle repairs, avoiding unexpected $5,000+ costs, and amenities like pools enhance quality of life without extra fees. In a low-sales market, renting avoids selling hassles if job changes arise. For this group, hybrid strategies—like rent-to-own programs—bridge the gap, but overall, renting suits transient phases, while buying rewards commitment.

For Lower-Income Individuals or Households: Prioritizing Accessibility and Security

At the lower end—households earning under $75,000, including service workers, young professionals, or single parents—renting overwhelmingly prevails in 2025 as the practical choice, given barriers to entry and ongoing affordability crises. In high-cost states like California, monthly home payments near $5,900 for typical properties, far exceeding rents averaging $1,636 nationally.

Renting’s Core Advantages: Low upfront costs (security deposit + first month’s rent, often $2,000-4,000) contrast sharply with buying’s $20,000+ down payment minimums. Flexibility aids job mobility in volatile economies, and subsidies like Section 8 vouchers cap rents at 30% of income. Maintenance is landlord-covered, preventing financial shocks, and community amenities provide value without ownership overhead.

Challenges of Buying: High rates amplify payments, and credit barriers exclude many. While programs like USDA loans offer 0% down in rural areas, equity building is slow, and appreciation isn’t guaranteed in depressed markets. Tax benefits exist but yield minimal savings in lower brackets.

Potential Pathways: For aspiring owners, affordable housing initiatives or co-ops lower barriers, but renting often preserves funds for education or emergencies.

Broader Market and Lifestyle Factors in 2025

Across all levels, 2025’s market favors renters short-term (cheaper in all 50 major metros) but buyers long-term, with projections of 4-5% home value growth through 2030. Stability suits families; flexibility, nomads. Amenities tilt toward renting in urban areas.

Decision Guide: Tailoring Your Choice

Assess finances (debt-to-income <36%), lifestyle (stay 5+ years? Buy), and research local trends. Consult calculators for break-even analysis.In 2025, buying builds legacies for the committed, while renting enables agility. Weigh your path carefully.

Disclaimer: The information provided here is for educational purposes only. It does not constitute investment advice or a guarantee of performance. Investing involves risks, including the possible loss of capital. Seek advice from financial and tax professionals tailored to your financial circumstances and goals.

See The Case Against the Credit Card Here